Also known as an in-law or mother-in-law unit, secondary dwelling unit, granny flat or backyard apartment, ADU’s are on the rise. There has been a significant increase in demand for ways to finance their construction in recent years, especially since changes to California law mean that it is now easier than ever to build one in a single-family zone.

In fact, municipalities across the US have relaxed previous restrictions on ADUs, and a number of states are now actively encouraging their development.

Los Angeles’ Mayor Eric Garcetti has even claimed that ADUs are a “way for homeowners to play a big part in expanding our city’s housing stock and make some extra money while they’re at it.”

But one of the most common obstacles that people face when planning this addition to their homes is financing the construction, especially given that the average cost of an ADU can come in anywhere between $100,000 and $300,000.

Alongside this is the fact that there is often a gap between the cost of the construction and a homeowner’s borrowing power when using traditional mortgage products, adding further complexities.

Finding the right way to finance a dwelling unit can be confusing, but it doesn’t need to be that way. Having access to the right type of financing could mean that you are able to design and build with a higher budget, especially when you consider the rental income it could bring in.

In this guide, we’ll walk you through each of your options and help you to understand the pros and cons of each one.

Specifically, we’ll cover:

How do I know if a RenoFi loan is right for my project?

The RenoFi team is standing by to help you better understand how RenoFi Loans work and the projects they are best suited for. Have a question - Chat, Email, Call now...

Understanding Your ADU Financing Options

The traditional options that are available to you for financing an ADU are typically based upon the amount of equity that you have available in your home, your household income, savings, and creditworthiness.

Alternatives do exist, however, that will let you borrow based on the future value of your home.

But one of the challenges often faced is the cost of construction and other associated fees, given that an ADU is so much more than a simple home renovation project. And for this reason, relying on equity or savings to cover these costs may result in the aforementioned gap between the budget you have available and the budget that you need.

That said, it’s important to also consider that one of the main differences between ADUs and other renovation projects is the rental income that they can bring.

Even when a dwelling unit is constructed in its entirety with borrowed funds, it can generate a positive return through rentals and increased property value in the future.

So let’s take a look at the financing options for dwelling units that are available to homeowners:

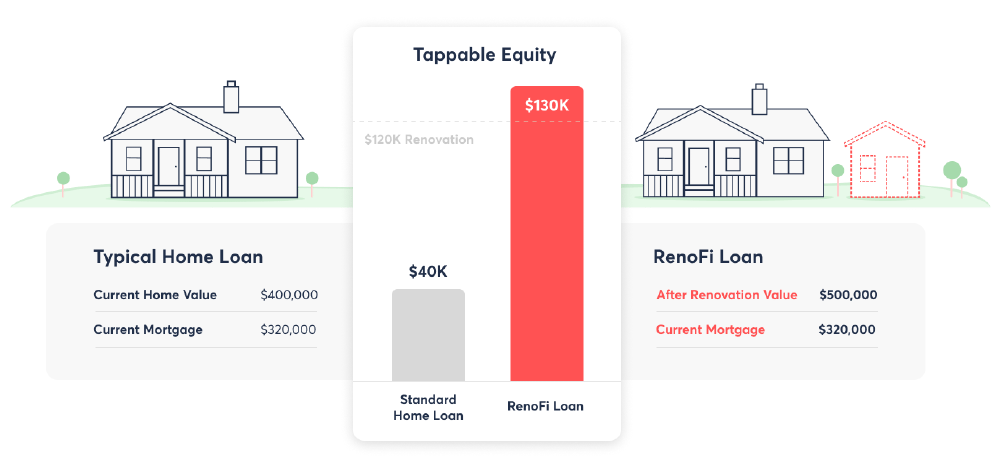

A RenoFi Loan

A RenoFi Loan is perfect for financing an ADU, given that it factors in what your home will be worth after construction is complete.

This, in turn, means that you can borrow all of the money you need at the lowest rate possible, overcoming the gap between borrowing power and available equity that many homeowners face.

A RenoFi Home Equity Loan gives the peace of mind of a fixed rate without the need to refinance your first mortgage, while a RenoFi Home Equity Line of Credit gives additional flexibility to draw what you need when you need it.

And RenoFi’s newest option - the RenoFi Cash-out Refinance - allows you to draw money from the equity of your new ADU to build it, while refinancing your primary mortgage.

The ability to borrow based on the value of your home after the addition of your ADU means that you can borrow more than what would be possible with other types of financing, even if you haven’t built up equity.

RenoFi Co-Founder and CEO Justin Goldman comments on this issue, stating: “Simply put, recent homebuyers are stuck between a rock and a hard place as it can take a decade or more to build up the equity needed to tackle their renovation wishlist.

“So what do homeowners do? 87% of them use cash - borrowing from retirement accounts, draining emergency savings, or borrowing from friends and family. Others rack up high-interest debt with personal loans and/or credit cards. And far too many begrudgingly reduce the scope of their project, tackling their renovation wishlist piecemeal over many years while living in a never-ending construction zone.”

Your house will go up in value with the addition of an ADU, and a RenoFi Loan can help you access this increase upfront to fund the construction.

A RenoFi Loan can often increase a homeowner’s borrowing power by 3x or more, while also ensuring the lowest possible rate.

Traditional HELOC (Home Equity Line of Credit) & Home Equity Loan

Financing the construction of an ADU using home equity is common. But if a homeowner doesn’t have sufficient equity to borrow against, this can present a problem.

Home Equity Loan

Home equity loans (also known as second mortgages) allow you to borrow a fixed amount of cash, backed by the equity that you have in your home, and repay it against an agreed upon schedule.

It is important to note that the interest rate payable on an equity loan will be higher than the rate on your first mortgage and will incur closing costs and other fees to cover an appraisal, lender fees, credit reports, etc.

HELOC

A HELOC (Home Equity Line of Credit) also allows you to borrow against the equity in your home and can provide a revolving line of credit (up to a set limit). In this case, interest is only payable (typically over a period of up to 10 years) on the cash that you have drawn on.

The interest rate incurred with a HELOC will be higher than on your first mortgage and is also likely to be a variable rate. The majority of lenders are willing to lend up to a maximum of between 80% and 85% of the value of your home (minus your first mortgage).

If you have recently purchased your home and have not built up much equity, either of these options will likely prevent you from borrowing the amount that you need for the construction of an ADU, creating a gap between your borrowing power and the cost of development.

Cash-Out Refinance

A cash-out refinance requires you to refinance your first mortgage and release some of the equity that has been built up in your home to finance the construction of your ADU.

While this option will consolidate the finance needed for construction and your first mortgage into a single loan, it again requires you to have built-up equity in your home. You will have much less borrowing power than with other options, with most cash-out refinances only letting you tap up to 80% of your home’s current value (unless you’re using a RenoFi Cash-out Refinance).

You’ll also face closing costs and higher rates than other financing options, essentially meaning that you’re throwing money away unless you’re significantly lowering your rate.

While someone who bought their home when interest rates were much higher (say in 2000) may find that this is a good move, some homeowners shouldn’t use cash-out refinance for renovations (including for the addition of ADUs).

A Construction Loan

Many people are wrongly steered in the direction of a construction loan for all kinds of home improvement projects, including the building of an ADU, for the simple reason that they help you to borrow based on the future value of your home.

And while a few years ago this might have been your best option for financing an ADU, this isn’t necessarily the case anymore.

In fact, we’ve written extensively about why you shouldn’t use a construction loan for your renovation.

While a construction loan may help homeowners who have less equity in their property to borrow the money they need to develop an ADU, they will need to refinance, and this can mean losing a great fixed rate (if this was locked in when these were at a rock-bottom low.

Construction loans will also face higher closing costs, based on the new value of the mortgage and budget, as well as adding a whole heap of additional work for both yourself and your contractor.

You see, construction loans were originally intended as a way to finance a new home build from the ground up, and stringent requirements were put in place by lenders as a method of protection.

As a result, this adds an extra layer of complexity to borrowing, such as your contractor being required to submit a draw schedule, arranging and waiting on inspections and a necessity to share continual updates with the lender.

Construction loans are a one-size-fits-all solution and are not based on your specific needs and requirements, meaning that there are likely better options to help you pay for building an ADU.

High-Interest Rate, Unsecured Personal Loans or Credit Card

Personal loans and credit cards are categorically not the most suitable approach to financing an ADU. These methods are unsecured and have high-interest rates. Yet homeowners often use this type of finance to pay for renovation work, due to the assumption that there are no alternatives, or to help plug the gap between their borrowing power and the equity that they can release.

You need a good credit score and a sizable household income to borrow on an unsecured personal loan or credit card, but regardless of this, we’re of the opinion that this type of high-interest rate borrowing is one of the dumbest things that homeowners do when paying for renovations and additions to their property.

It’s Time to Feel Inspired

Knowing that you’ve found the perfect solution for financing an ADU is a huge weight off your shoulders.

In fact, securing the funds to start construction means you can start to have conversations with contractors and architects who can realize your vision.

But it always pays to dream big and take the time to inspire and immerse yourself in the projects other people have shared for the rest of the world to see.

And to help get you thinking about what could be possible, we love Houzz’s outbuildings ideabook and ADU ideas & photos collection, as well as Pinterest (of course!) and Dwell’s round up of 29 Granny Flats That Put Guests Up in Style.”

FAQs on Financing an ADU

Is adding an ADU a good investment?

Does an ADU add value to your home?

What is the best way to finance an ADU?

What financing options exist to build an ADU?

Financing Shouldn’t Be the Hardest Part of Building an ADU … RenoFi Can Help

The prospect of building an ADU should be an exciting one, but the unfortunate reality for many is that financing typically adds another layer of complexity to the process.

But RenoFi can help.

How do I know if a RenoFi loan is right for my project?

The RenoFi team is standing by to help you better understand how RenoFi Loans work and the projects they are best suited for. Have a question - Chat, Email, Call now...